Planning a Life When the Numbers Never Feel Safe

You did the things you were supposed to do. You built up some savings. You paid down a credit card or two. You started a retirement contribution, even a small one. On paper, the numbers are not catastrophic. Maybe they are even okay.

And yet the anxiety is still there. The low-level hum of financial worry that does not go away when the balance goes up. The compulsive checking of the account you already checked an hour ago. The inability to make a major decision — buy a car, move to a new city, have a child — without the gnawing feeling that the numbers will never be safe enough to proceed.

📌 For a broader look at building long-term security, see our complete guide to financial stability.

If this sounds familiar, you are not alone, and you are not irrational. Financial anxiety that persists beyond what the numbers justify is one of the most common and least-discussed experiences in personal finance. Understanding where it comes from — and how to plan your life despite it — is as important as any budgeting tactic.

Why the Numbers Never Feel Safe Enough

The financial anxiety many people carry is not proportional to their account balance. People with healthy savings still lose sleep over money. People who are technically stable still feel one unexpected bill away from collapse. This is not a character flaw or a failure of financial knowledge. It is, in large part, an emotional response shaped by experience.

For many adults today, early money experiences were marked by instability. Growing up in a household where money was tight, where bills were a source of stress and argument, where financial surprises were always bad — these experiences leave a lasting imprint. Psychologists call this financial trauma: a persistent nervous system response to money that treats even current stability as fragile and temporary.

The brain does not easily distinguish between a past threat and a present one. If money meant danger at some point — the lights being shut off, a parent’s panic, a sudden move — that association does not simply reset when your savings account crosses a threshold. It persists. It watches. It waits for the other shoe to drop.

Research in behavioral economics adds another layer. Studies consistently show that losses feel roughly twice as painful as equivalent gains feel good — a phenomenon called loss aversion. Even when you are financially stable, the fear of losing what you have can outweigh the comfort of having it. This is not weakness. It is how human brains are wired, particularly in the context of scarcity or past loss.

How Financial Anxiety Shows Up in Real Life

Financial anxiety rarely announces itself clearly. Instead, it shapes behavior in subtle, often counterproductive ways.

It shows up as avoidance — not opening bills, not looking at bank statements, not doing the annual insurance review because you dread what you might find. Avoidance feels like relief in the moment, but it allows problems to grow unseen.

It shows up as compulsive monitoring — checking your balance multiple times per day, refreshing investment apps during market dips, running the same numbers over and over as though the answer will change. This kind of checking creates an illusion of control but actually amplifies anxiety by keeping financial worry constantly present in your mind.

It shows up as paralysis — the inability to make a financial decision even when the information supports it. You research the decision endlessly. You ask for more data. You wait for certainty that never arrives. Meanwhile, the question of whether to refinance, invest, or move stays perpetually unresolved.

And it shows up in major life decisions. The couple who delays having children because the numbers never feel quite right. The person who stays in a job they dislike because the security feels too valuable to risk. The renter who cannot bring themselves to buy, not because they cannot qualify, but because the commitment feels terrifying when financial stability feels so precarious.

Recognizing these patterns — in yourself — is the first step toward loosening their grip. It is also worth understanding why financial anxiety feels worse than the numbers, because the emotional experience of financial stress is its own phenomenon, separate from the math.

When Digital Tools Make It Worse

Modern personal finance technology was supposed to reduce financial anxiety by providing clarity and control. For many people, it has done the opposite.

Budget apps send push notifications about every transaction. Investment platforms display real-time market fluctuations in dramatic red and green. Retirement calculators project your 2055 nest egg to the dollar, then update it daily based on market movement. The result is not calm — it is a constant stream of financial data points demanding attention and generating anxiety.

This is not the tools’ fault, exactly. It is a mismatch between what the tools were designed to do and what anxious minds do with them. For someone with financial anxiety, more data does not produce more confidence. It produces more variables to worry about, more numbers that could go wrong, more evidence that certainty is impossible.

A 2024 survey by the Financial Health Network found that adults who reported high financial stress checked their accounts an average of five or more times per week — and that more frequent checking correlated with higher anxiety, not lower. The checking itself feeds the loop rather than resolving it.

If you notice that your financial apps are triggering anxiety rather than helping you manage it, that is useful information. The tools are working as designed — you may simply need to use them differently. More on that in the practical section below.

Financial Safety Is a System, Not a Number

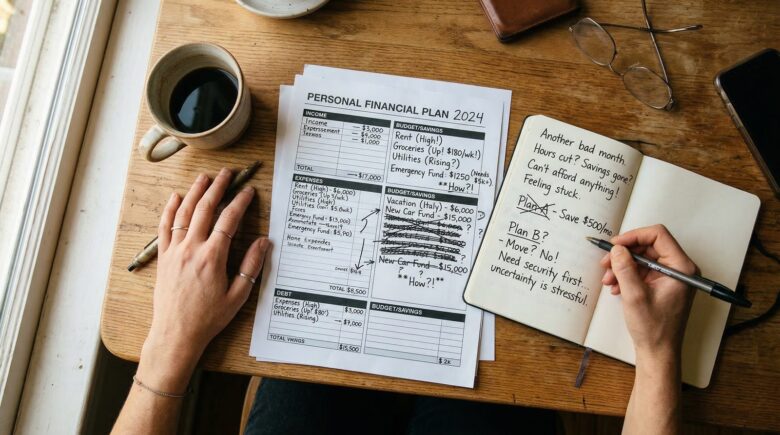

One of the most common traps in financial anxiety is the moving threshold: the belief that safety begins at some specific number, and the quiet discovery, once you reach it, that the anxiety has simply moved the target further out. When you had $500 in savings, $1,000 felt like enough. When you got to $1,000, $5,000 became the benchmark. When you hit $5,000, suddenly it is three months of expenses. Then six. Then a year.

The threshold keeps moving because financial security is not actually a number. Numbers provide concrete benchmarks, and benchmarks matter — but no amount of money eliminates all financial risk. Emergencies happen. Economies shift. Health changes. The pursuit of a number large enough to feel finally safe is, in a meaningful sense, a pursuit that never ends.

A more sustainable framework is thinking of financial security as a system rather than a balance. The system includes: an emergency fund that absorbs shocks. Debt at a manageable and declining level. Income that covers expenses with some margin. Insurance that limits catastrophic loss. And enough financial flexibility to adapt if circumstances change.

When you ask not “is this number big enough?” but “does my financial system handle uncertainty well enough to move forward?” — the question becomes more answerable. A robust system can absorb imperfection. It provides a kind of durability that any single number, by definition, cannot.

How to Plan Major Life Decisions Without Perfect Conditions

Major life decisions — buying a home, changing careers, starting a family, going back to school — are almost never made under perfect financial conditions. They are made under “good enough” conditions, with contingency plans and an honest assessment of what you can handle if things do not go as expected.

Waiting for financial certainty is, functionally, a way of never deciding. The goalposts move. Life does not pause while you accumulate one more month of savings or wait for the market to settle. And many of life’s most important choices have a time dimension that cannot be deferred indefinitely.

Scenario planning as a substitute for certainty

Instead of asking “Is this financially safe?” try asking “Can I handle the realistic worst-case scenario?” Work through the specific downside: What if we buy the house and I lose my job six months later? What happens next? The answer might reveal that you would need to draw on savings for three months while finding new work — and that is manageable. Or it might reveal a gap you can address before moving forward. Either way, you replace vague dread with a concrete problem you can plan around.

Recognizing what is reversible

Financial anxiety tends to experience decisions as more permanent than they are. In reality, most financial decisions are partially or fully reversible. A house can be sold. A car can be traded. A job can be left. A budget category can be cut. Recognizing that most choices do not permanently lock you in reduces the psychological stakes of making them — and helps move decision paralysis toward action.

Distinguishing anxiety from genuine risk signal

Not all financial hesitation is anxiety-driven. Sometimes the numbers genuinely are not ready, and the discomfort is a real signal that deserves attention. The difference: if you can identify the specific risk — “I do not yet have enough saved to cover a down payment and maintain an emergency fund” — that is a concrete, addressable concern. If the worry is more diffuse — “what if something goes wrong that I cannot predict?” — that is anxiety asking for reassurance that no amount of preparation will provide.

Setting Boundaries With Financial Monitoring

If compulsive account-checking is part of your anxiety pattern, deliberate limits help more than willpower. Here are approaches that work for many people:

- Scheduled check-ins only: Choose specific times — once a week, or twice — to review your accounts. Outside those times, the app stays closed. This preserves awareness without feeding the checking loop.

- Delay notifications: Turn off real-time transaction alerts and review spending in a weekly batch instead. The information is the same; the anxiety is lower without constant pings.

- Separate monitoring from action: Looking at your accounts and feeling anxious is not the same as a problem requiring action. Building the habit of observing without immediately reacting reduces the reactive quality of financial anxiety.

- Net worth check quarterly, balance check weekly: Check what matters at the right cadence. Daily investment balance checks serve no real purpose for long-term investors and produce significant anxiety. Quarterly is enough for retirement accounts.

Building Emotional Safety Alongside Financial Safety

Financial therapy — a growing field that combines financial planning with psychological support — starts from the premise that money problems are often emotional problems wearing financial clothes. The behavior that produces financial difficulty frequently has roots in anxiety, avoidance, scarcity thinking, or unresolved money beliefs from childhood.

You do not need a therapist to start doing this work. But it helps to approach financial decisions with awareness of your own patterns. If you tend toward avoidance, build systems that reduce the need to face money directly — automation, scheduled reviews, accountability with a partner. If you tend toward compulsive monitoring, build constraints that limit access. If you tend toward paralysis, build a practice of making small financial decisions quickly and noticing that the outcomes are usually fine.

Understanding the quiet shame people carry about money — and where it comes from — is often part of loosening its grip. And exploring why being bad with money is often a systems problem rather than a character flaw can shift the lens from self-judgment to problem-solving.

Planning Ahead Without Waiting for Safe

The numbers will probably never feel completely safe. For people with a history of financial anxiety, safety is not primarily a financial condition — it is an emotional one. And emotional safety around money is built through experience, through demonstrating to yourself over time that you can navigate uncertainty, make decisions under imperfect conditions, and recover from setbacks.

You build it by making the decision, watching the outcome, and surviving the discomfort. You build it by discovering that the worst case, when it happens, is usually more manageable than the anticipation. You build it by creating a financial system that is genuinely resilient — not one that eliminates all risk, but one that handles risk well enough to move forward.

Perfect conditions are not required. A solid-enough financial foundation, an honest assessment of what you can handle, and a willingness to adapt as circumstances change — these are sufficient for most major life decisions. The spreadsheet will never provide the reassurance you are looking for. That reassurance comes from building your capacity to handle what you cannot fully predict. And that capacity grows one decision at a time.

Related Reading

- What Financial Stability Actually Looks Like

- When Financial Progress Feels Invisible

- Emergency Funds Are Boring — And That’s the Point

Frequently Asked Questions

Why does financial anxiety persist even when my finances are actually okay?

Financial anxiety often has deeper roots than current account balances — in past experiences of scarcity, family money stress, or economic uncertainty witnessed in formative years. The brain treats past financial threat as an ongoing one, keeping a vigilance that does not automatically turn off when the numbers improve. This is a normal psychological response, not a failure of rationality.

How do I know if financial hesitation is a real warning sign or just anxiety?

Ask yourself: can I name the specific risk? If the concern is concrete and addressable — “I need three more months of savings before this makes sense” — it deserves attention. If it is diffuse and never quite satisfied regardless of the numbers — “I just don’t feel safe enough” — that is more likely anxiety seeking reassurance that no number will provide. The former calls for action; the latter calls for a different kind of work.

Is it possible to make good financial decisions while still feeling anxious?

Yes — and for many people, that is the only available option. The goal is not to eliminate anxiety before acting; it is to act thoughtfully despite anxiety. Scenario planning, honest risk assessment, and building reversibility into major decisions all make it possible to move forward without requiring certainty first.

What does a “safe enough” financial foundation actually look like for making a big decision?

A reasonable foundation for major decisions typically includes: a functioning emergency fund covering at least one to two months of essential expenses; no high-interest consumer debt that would be worsened by the new commitment; income that comfortably covers current obligations with some margin; and a rough contingency plan for the realistic worst case. This is not certainty — it is readiness. Most major life decisions do not require more than this.

Dana Whitfield is a financial therapist and writer who explores the emotional side of money. With a background in behavioral psychology and over a decade of work in community financial counseling, she helps readers understand why money feels the way it does — and what to do about it. She writes from Chicago, IL.