| JA James Achebe | 🕓 7 min read | Updated Mar 16, 2026 |

Fact-checked by the Visual eNews editorial team | Our editorial standards

Someone you care about has asked you to cosign a loan. Maybe it’s your child buying their first car. Maybe it’s a sibling who needs an apartment lease. Maybe it’s a close friend who just needs a little help qualifying. It feels like a simple favor — your signature, their loan, no money out of your pocket.

📌 For a broader look at building long-term security, see our complete guide to financial stability.

Except that’s not how it works. When you cosign, you’re not vouching for someone’s character. You’re legally guaranteeing their debt. And according to a CreditCards.com survey reported by Forbes, roughly 4 in 10 cosigners end up having to pay some or all of the loan themselves — and about a third saw their own credit scores drop as a result. This isn’t a rare worst case. It’s what happens to a significant percentage of people who sign on the dotted line.

★ Key Takeaways

- ✓Cosigning means you’re 100% liable for the full debt — legally, there is no difference between you and the borrower in the eyes of the lender.

- ✓About 38% of cosigners end up paying some or all of the loan, and 28% experience a credit score drop from missed payments they didn’t make.

- ✓The cosigned loan immediately increases your debt-to-income ratio, which can prevent you from qualifying for your own mortgage, auto loan, or credit card.

- ✓Alternatives exist: secured cards, credit-builder loans, secured loans, and federal student loans don’t require a cosigner at all.

What Cosigning Actually Means — Legally

There’s a widespread misconception that cosigning is like writing a letter of recommendation. It’s not. When you cosign a loan, you become a co-borrower in the eyes of the lender. The full loan balance appears on your credit report, the payment history affects your score, and if the primary borrower stops paying, you owe every dollar plus interest and late fees.

The Federal Trade Commission requires lenders to provide a “Notice to Cosigner” that begins with: “You are being asked to guarantee this debt. Think carefully before you do. If the borrower doesn’t pay the debt, you will have to.” That’s the federal government telling you, in writing, that this is serious.

A cosigner is different from a co-borrower or co-applicant. A co-borrower shares in the proceeds — like a spouse on a mortgage. A cosigner receives no benefit from the loan. They’re purely a guarantor. That distinction matters legally, but practically, the financial liability is identical.

The Five Real Risks

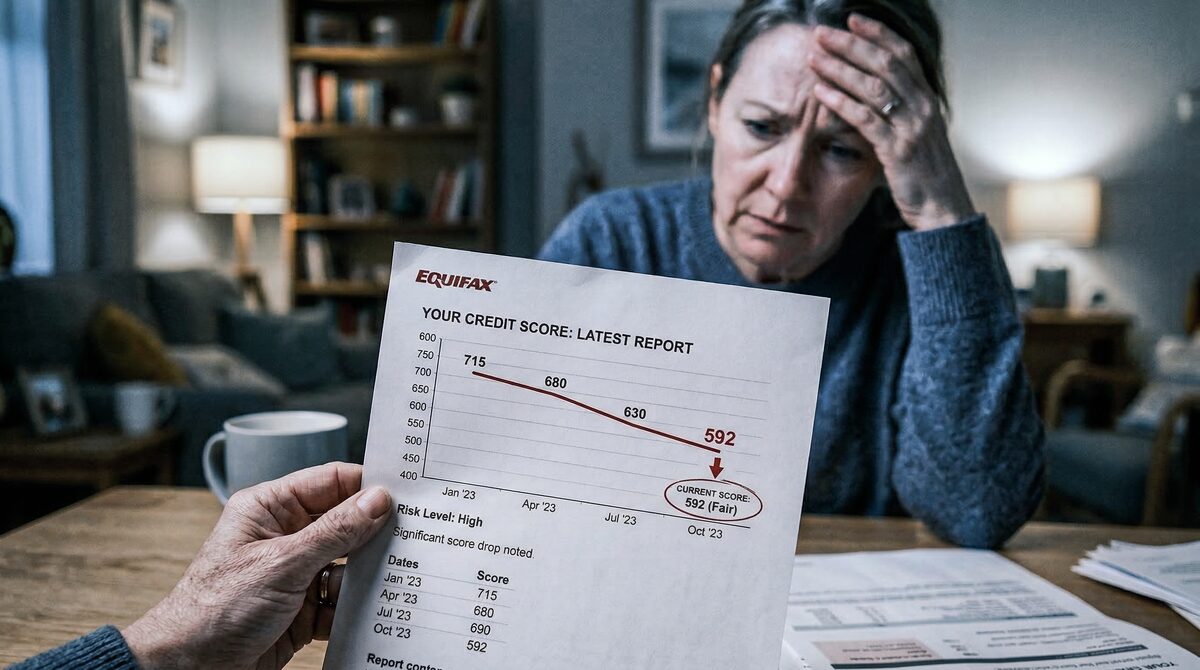

1. Your credit score takes every hit the borrower causes. Late payments, missed payments, defaults — they all land on your credit report. Payment history accounts for 35% of your FICO score. A single 30-day late payment can drop a good score by 60–100 points, and that mark stays on your report for seven years, according to Experian.

2. Your borrowing power shrinks immediately. The cosigned loan counts toward your debt-to-income ratio from day one. If you cosign a $25,000 car loan with a $450 monthly payment, lenders see that as your $450 obligation. That can be the difference between qualifying for a mortgage and getting denied.

3. You can be sued — directly. If the borrower defaults, the lender or a collection agency can take legal action against you for the full balance. In most states, the lender doesn’t need to exhaust options with the primary borrower first. They can come to you immediately.

4. Getting out is extremely difficult. Most loans have no cosigner release mechanism. The CFPB found that 90% of private student loan borrowers who applied for cosigner release were rejected. For auto loans and personal loans, the only exit is typically refinancing — which requires the primary borrower to qualify on their own.

5. It can destroy relationships. A CreditCards.com survey found that 26% of cosigners said the experience damaged their relationship with the borrower. Money stress between family members hits differently than a credit card bill — it carries shame, resentment, and a kind of betrayal that’s hard to undo.

What to Do If You’ve Already Cosigned

If you’re already on the hook, don’t panic — but do take action now rather than waiting for problems to surface.

Monitor the loan actively. Ask the lender for online account access or request that statements be sent to you directly. You need to know about missed payments before they hit 30 days and damage your credit. Don’t rely on the borrower to tell you there’s a problem.

Push for refinancing. If the borrower’s credit has improved since the original loan, they may be able to refinance into their own name — removing you from the obligation entirely. This is the cleanest exit and should be the goal from day one.

Know your state’s protections. Some states have additional cosigner protections. In Michigan, for example, the lender cannot report adverse information about the cosigner to credit bureaus until they’ve notified the cosigner of the default and waited at least 30 days. Check with your state attorney general’s office.

Set up payment alerts on the cosigned account. Many lenders allow text or email notifications when a payment is due or missed. This gives you a window to step in before a late payment gets reported to the credit bureaus — typically at the 30-day mark.

Alternatives That Don’t Put Your Credit on the Line

If someone you care about needs help getting credit, cosigning is rarely the only option — and it’s almost never the best one.

The authorized user approach is particularly worth considering. It gives the person credit-building benefit while you retain full control — you can set spending limits, monitor activity, and remove them instantly if needed. It’s the closest thing to helping without risking your own financial standing.

When Cosigning Might Actually Make Sense

This article isn’t here to tell you never to cosign. There are situations where it genuinely makes sense — but they require specific conditions.

You can afford to pay the entire loan yourself. This is the first and most important test. If you couldn’t absorb the full monthly payment without financial strain, cosigning is too risky regardless of how trustworthy the borrower seems.

You have a written agreement. Before signing anything with the lender, create a private agreement with the borrower that covers: who pays what, what happens if payments are missed, a plan and timeline for refinancing you off the loan, and how you’ll monitor the account.

There’s a clear exit timeline. Cosigning should have an expiration date. The borrower should be actively building credit with the goal of refinancing within 12–24 months. If there’s no plan to get you off the loan, there’s no plan at all.

The FTC’s Credit Practices Rule legally requires lenders to give you a formal “Notice to Cosigner” before you become obligated — except for most real estate loans, which are exempt from this requirement. If a lender skips this notice, they may be violating federal law.

Frequently Asked Questions

Can I remove myself as a cosigner?

In most cases, you cannot unilaterally remove yourself. The primary borrower would need to refinance the loan in their own name, or the lender would need to offer a cosigner release program — which are rare and have high rejection rates. The CFPB found that 90% of cosigner release applications for private student loans were denied.

Does cosigning affect my ability to get a mortgage?

Yes. The cosigned loan appears on your credit report as your debt. Mortgage lenders include that payment in your debt-to-income ratio calculation. If the cosigned debt pushes your DTI above the lender’s threshold (typically 43% for most mortgages), you could be denied.

What happens if the borrower files for bankruptcy?

If the primary borrower discharges the debt through bankruptcy, you — as the cosigner — still owe the full balance. The borrower’s bankruptcy does not release you from liability. Some private student loan contracts even trigger an auto-default if the cosigner (not the borrower) files for bankruptcy or dies.

Is cosigning a car loan different from cosigning a student loan?

The basic liability is the same, but the details differ. Car loans are secured by the vehicle — the lender can repossess the car, but if it sells for less than the balance, you still owe the difference. Student loans (especially private ones) have fewer protections and longer terms, making cosigner release even harder to obtain.

Should I cosign for my child?

Only if you can genuinely afford to make the payments yourself and you’ve exhausted alternatives. For student loans, federal loans don’t require a cosigner and offer income-driven repayment plans. For a first car, consider a less expensive vehicle the borrower can finance alone, or help with a larger down payment instead.

Sources

- Federal Trade Commission — Cosigning a Loan FAQs

- Forbes / CreditCards.com — Here’s How Often Co-signers Get Burned

- Consumer Financial Protection Bureau — 90% of Co-Signer Release Applications Rejected

- Experian — What to Do if You Cosign and Someone Defaults

- FTC Credit Practices Rule — Complying with the Credit Practices Rule

- Nasdaq — 7 Hidden Financial Risks of Being a Cosigner